.png)

The Future of Fintech Security: Stripe's AI-Powered Payment Protection

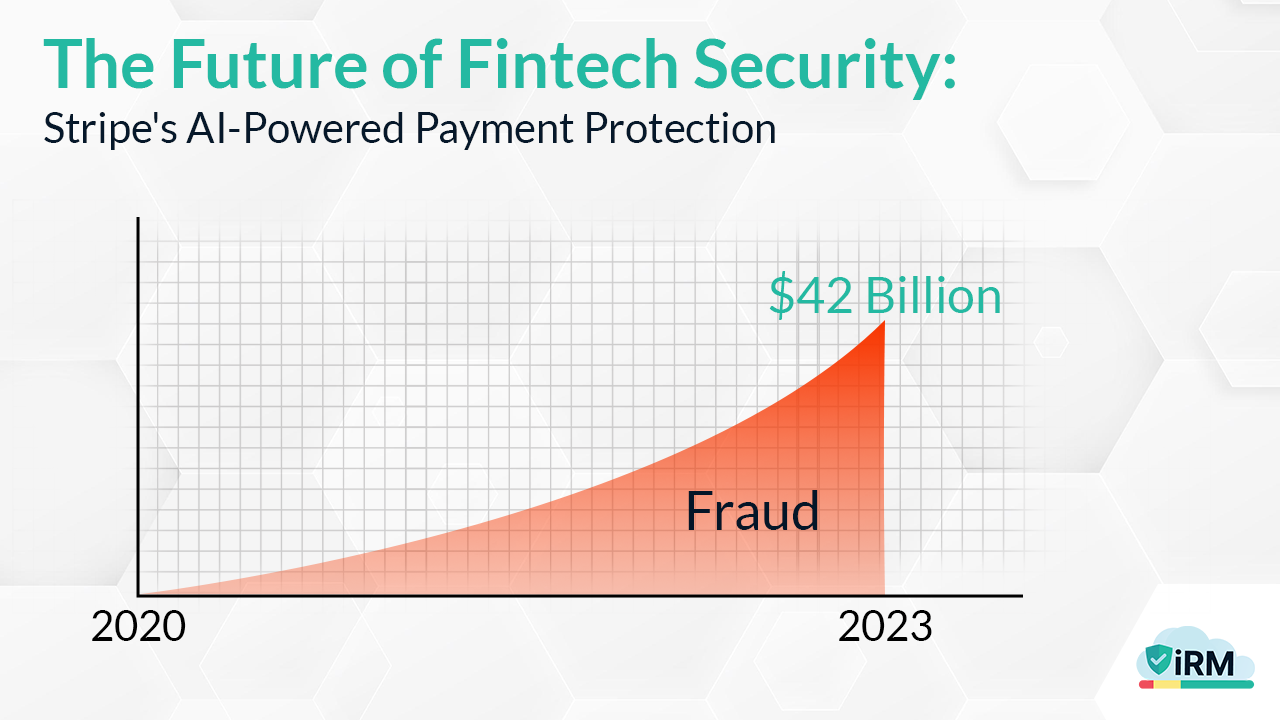

The Fraud

Hey there! Did you know that payment fraud is costing businesses a whopping $42 billion annually? That's right—fraudsters are getting smarter and more sophisticated by the day. And it's not just small businesses that are suffering; even giants like Stripe have faced significant challenges.

Between 2020 and 2023, Stripe saw a 40% surge in fraudulent transactions. That's a huge problem when you're handling payments for millions of businesses worldwide. But here's the good news: Stripe didn't just sit back and take it. They fought back with AI-powered Governance, Risk, and Compliance (GRC) tools—and the results have been nothing short of impressive.

In this blog, we'll dive into how Stripe transformed its approach to payment fraud using AI-GRC, what specific strategies they implemented, and how you can apply similar solutions to protect your business. Let's get started!

The True Cost of Payment Fraud

Payment fraud isn't just about losing money directly from fraudulent transactions. The hidden costs can be devastating for businesses. Did you know that the average cost per fraudulent transaction is $143? That's not including the reputational damage when customers lose trust in your payment systems.

What's more concerning is the 35% increase in cross-border fraud transactions. As businesses expand globally, fraudsters are finding new ways to exploit vulnerabilities. Fintech companies, in particular, face unique challenges. Their rapid growth creates more attack surfaces, and customers expect seamless, frictionless experiences—making it harder to implement traditional security measures without affecting user experience.

Let's break down the true cost of payment fraud:

• Direct financial losses: The most obvious cost is the money stolen through fraudulent transactions. For large businesses, this can amount to millions annually.

• Operational costs: The time and resources spent investigating fraudulent transactions, reversing charges, and dealing with chargebacks.

• Reputational damage: Once customers lose trust in your payment security, they may take their business elsewhere.

• Regulatory penalties: Non-compliance with payment security standards can result in significant fines.

• Customer acquisition costs: Losing customers due to security concerns means you have to spend more to acquire new ones.

Traditional Fraud Detection Methods

Let's take a quick look at how fraud detection worked before AI came into the picture. Rule-based systems were the go-to solution. These systems used predefined criteria to flag suspicious activity. For example, a transaction above a certain amount or from a high-risk location would trigger an alert.

The problem? These systems were rigid and couldn't adapt to new fraud patterns. They also generated a lot of false positives, meaning legitimate transactions were incorrectly flagged as fraudulent. This led to frustrated customers and time-consuming manual reviews.

Manual review processes were another cornerstone of traditional fraud detection. Teams would manually investigate flagged transactions, which was time-consuming and resource-intensive. With the volume of transactions growing exponentially, this approach simply couldn't scale.

AI-Powered GRC: The Modern Solution

So, what exactly is GRC in the context of fintech? GRC stands for Governance, Risk Management, and Compliance. It's a framework that helps organizations manage their operations effectively while adhering to regulations and minimizing risks.

AI has revolutionized GRC by bringing machine learning, real-time data processing, and adaptive decision-making to the table. Unlike traditional systems, AI-GRC frameworks can learn from new data, adapt to changing patterns, and make predictions in real-time.

The key components include machine learning models that recognize patterns humans might miss, real-time processing capabilities that analyze transactions as they happen, and decision-making engines that can take immediate action when fraud is detected.

Stripe's AI Implementation Strategy

Stripe's journey to AI-powered fraud detection began with acknowledging their limitations. Their manual review backlog reached 120,000 cases per month, and customer trust metrics were dropping.

They partnered with specialized AI solutions providers to develop custom machine learning models tailored to their specific payment patterns. The implementation was phased, starting with high-risk transaction categories and gradually expanding across their entire platform.

Their technology stack includes TensorFlow for building machine learning models, AWS for scalable cloud infrastructure, and Python for analytics. This combination allows them to process massive amounts of data quickly and efficiently.

How Stripe's AI Algorithms Work

The magic happens in how Stripe's AI algorithms analyze transactions in real-time. They look at transaction velocity—how quickly multiple transactions occur from the same account—and geolocation patterns to detect impossible travel scenarios.

For synthetic fraud prevention, their AI analyzes behavioral biometrics, such as how a user interacts with their device, and uses network analysis to identify fraud rings. The algorithms continuously learn from new data, improving their accuracy over time.

Measurable Results and ROI

The results speak for themselves. Stripe achieved a 60% reduction in fraud losses and a 45% decrease in manual review workload. They saved an estimated $1.2 billion in potential fraud transactions in 2023 alone.

Customer trust improved dramatically with a 32% increase in Net Promoter Score (NPS) and a 48% reduction in chargebacks. Transactions are now approved faster, enhancing the overall user experience.

Beyond Fraud Prevention

The benefits extend far beyond just stopping fraud. Stripe saw operational efficiency gains with 35% faster transaction processing and significant resource reallocation to strategic initiatives.

They've also gained a competitive edge in the market, becoming known for their robust security measures. This has allowed them to attract high-risk merchant categories that other payment processors might avoid.

Challenges and Considerations

Implementing AI-GRC isn't without its challenges. Data privacy remains a top concern, especially with regulations like GDPR and CCPA. Stripe had to implement rigorous anonymization techniques and maintain transparent communication with customers about data usage.

Model bias is another consideration. AI systems can perpetuate biases if not carefully monitored. Stripe implemented regular bias audits and maintained human oversight in the decision-making process.

Let's look at the main challenges:

• Data privacy concerns: Balancing the need for comprehensive data with customer privacy expectations.

• Model bias mitigation: Ensuring AI systems don't develop discriminatory patterns.

• Implementation costs: The initial investment in AI infrastructure can be substantial.

• Regulatory compliance: Keeping up with changing regulations across different jurisdictions.

• Technical expertise: Finding team members with the right skills to develop and maintain AI systems.

The Future of AI in Risk Management

Looking ahead, AI in risk management will continue to evolve. We can expect to see AI-driven regulatory compliance becoming standard, with systems automatically adjusting to changing regulations.

Quantum computing integration could revolutionize how we process and analyze massive datasets. Global fraud prevention networks might emerge, allowing organizations to share threat intelligence in real time.

Ready to future-proof your business? iRM's experts can design a tailored AI-GRC strategy addressing your needs. Our team has helped numerous companies implement solutions that protect against fraud while maintaining customer trust.

Contact us today for a free 30-minute consultation and discover how intelligent risk management can become your competitive edge. Don't let fraud steal your growth—let iRM secure your future!